Type : Function, Name : jtHMA

Inputs: price(NumericSeries), length(NumericSimple);

Vars: halvedLength(0), sqrRootLength(0);

{

Original equation is:

———————

waverage(2*waverage(close,period/2)-waverage(close,period), SquareRoot(Period)

Implementation below is more efficient with lengthy Weighted Moving Averages.

In addition, the length needs to be converted to an integer value after it is halved and

its square root is obtained in order for this to work with Weighted Moving Averaging

}

if ((ceiling(length / 2) — (length / 2)) <= 0.5) then

halvedLength = ceiling(length / 2)

else

halvedLength = floor(length / 2);

if ((ceiling(SquareRoot(length)) — SquareRoot(length)) <= 0.5) then

sqrRootLength = ceiling(SquareRoot(length))

else

sqrRootLength = floor(SquareRoot(length));

Value1 = 2 * WAverage(price, halvedLength);

Value2 = WAverage(price, length);

Value3 = WAverage((Value1 — Value2), sqrRootLength);

jtHMA = Value3;

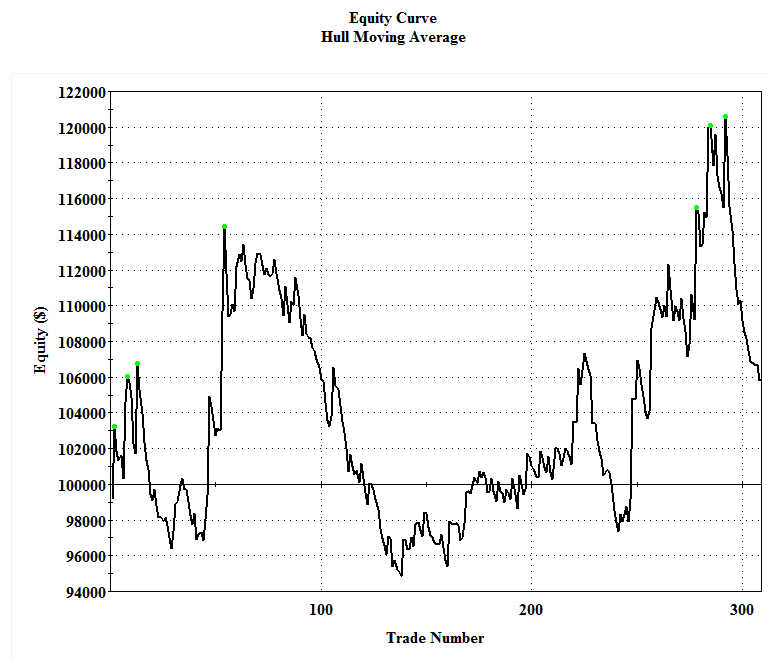

Type : System, Name : Hull Moving Average Trading System

inputs: price(Close), jthmaLength( 21 ), upColour(Blue), downColour(Red);

variables: Avg(0), colour(0);

Avg = jthma( price, jthmaLength ) ;

if Avg > Avg[1] then colour = upColour;

if Avg < Avg[1] then colour = downColour;

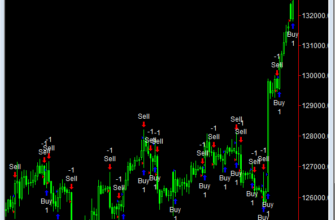

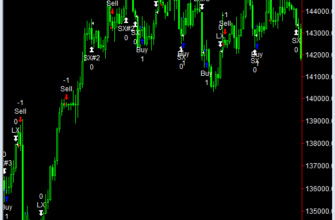

{buy sell Criteria}

if colour[1] <> colour then

if colour = upColour then

Buy ( «jup» ) next bar at market ;

if colour[1] <> colour then

if colour = downColour then

sell ( «jdn» ) next bar at market ; {original this line is: sell short ( «jdn» ) next bar at market ; }